Our SGIP Incentives are Live on the Platform

by Jared DeRemer on Feb 01, 2018

energy storage

project development

SGIP

The Self-Generation Incentive Program (SGIP) provides financial incentives for the installation of new, qualifying technologies including energy storage, wind power, fuel cells, combined heat & power and others. It was big news when the program relaunched in the spring of 2017, with a re-upped program budget that was earmarked primarily for customer-sited Energy Storage Systems (ESS).

Calculating SGIP incentives can be tricky, as the incentive amount is dependent on several different system variables. In Energy Toolbase we recently launched our new SGIP global incentives, which were built to be fully dynamic, meaning they should calculate correctly for any scenario. Below is a list of variables that dictate how the SGIP incentive will be calculated.

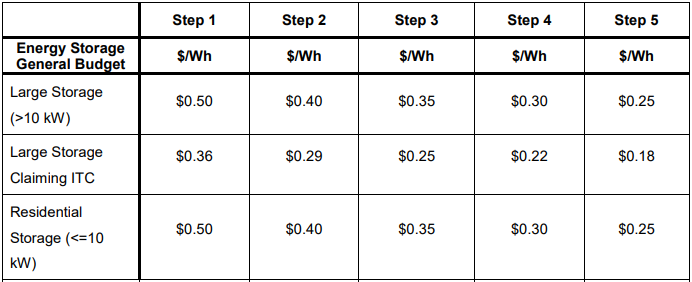

Energy Storage Incentives per Watt-hour (Wh):

If an incentive step becomes fully subscribed in all Program Administrator territories within 10 calendar days, the following step will decrease by $0.10/Wh. Note: the table above has been updated to reflect an accelerated incentive decline of $0.10/Wh in step 2.

Small storage systems or Large storage systems:

There are two categories within the energy storage general budget, which operate independently of each other. “Small residential storage” systems (< 10 kW), and “Large-Scale storage” systems (> 10 kW). Of the total SGIP budget, 80% is allocated to energy storage technologies, with 15% set aside for “small residential storage” projects.

California Supplier – 20% adder:

For projects utilizing equipment manufactured in California, an additional incentive of 20 percent will be added to the project. For a project to qualify for the 20 percent addition, the technology must demonstrate that at least 50% of its capital equipment value is manufactured by an approved California Manufacturer.

With or without an Investment Tax Credit (ITC):

“Large-scale” Energy Storage Systems claiming a federal Investment Tax Credit will receive a reduced SGIP incentive amount, as specified in the table above. The reduction in SGIP incentive when claiming an ITC is equivalent to roughly 28%, depending on the incentive step. To be considered paired with, and charging from on-site renewables, an ESS must charge a minimum of 75% from the on-site renewable generator.

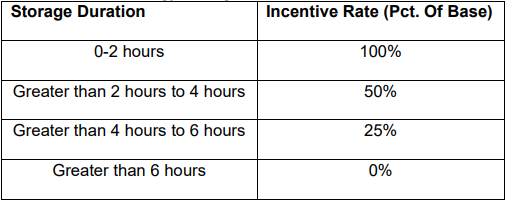

Incentives Decline based on Storage Duration:

SGIP incentives are reduced as the duration of ESS capacity (kWh) increases in relation to the ESS rated power (kW), according to the following schedule:

Performance-Based Incentive (PBI) payments:

For ESS projects 30 kW and larger, 50% of the incentive will be paid upfront and the remaining 50% will be paid as a performance-based incentive (PBI) over a 5-year period. Annual PBI payments will be structured so that under the expected annual operational requirements (130 full dischargers per year), a project would receive the entire stream of PBI payments in five years. To calculate the basis ($/kWh) of the annual PBI payments the following calculation is made:

$/kWh = remaining 50% of incentive / total anticipated kWh discharge

Total anticipated kWh discharge = energy capacity (kWh) * 130 full discharges * 5 yrs

Note: if the ESS cycles more than 130 full discharges per year, the SGIP incentive can be captured in less than 5-years.

Final thoughts:

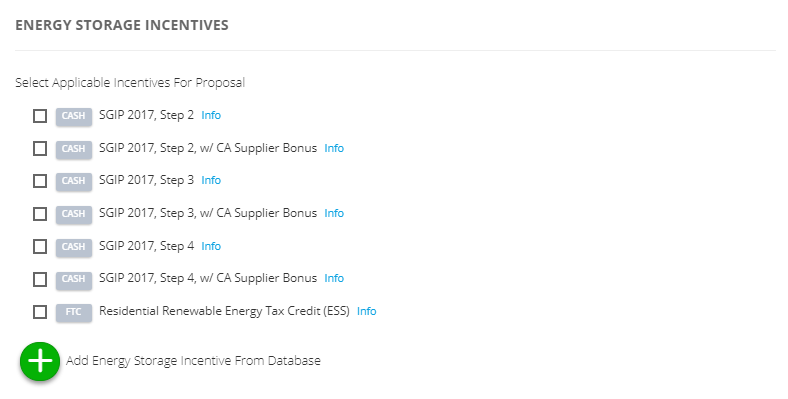

For the time being, we’ve “Activated” step 2, 3, 4 SGIP incentives, meaning these will be displayed as selectable ESS incentives in “Step 3 – Incentives”.

You can use this blog as a guide to determine how we dynamically calculate SGIP incentives based on different types of configurations and assumptions. As with all global incentives in our database, users can view our written logic, which dynamically calculates these incentives.

Jared DeRemer is a software engineer for Energy Toolbase, based in Stuart, Florida.