*Updated on 11/18/2019 to reflect the correction that the full 30% tax credit applies only to commercial projects that commence construction before 1/1/2020 and the full 30% applies only to residential projects placed in service (PIS) by 1/1/2020*

The Federal Investment Tax Credit (ITC) has unquestionably been the most important federal policy mechanism to incentivize renewable energy projects in the US over the last decade and a half. The ITC was originally established by the Energy Policy Act of 2005. “Since the ITC was enacted the U.S. solar industry has grown by more than 10,000%” according to the Solar Energy Industry Association (SEIA).

Both the residential and commercial tax credit is currently equal to 30% of the basis that is invested in eligible solar or storage projects. A tax credit is effectively a dollar-for-dollar reduction in the income taxes that a person or company would otherwise pay the federal government. To claim and receive the full 30% tax credit the system owner must owe at least as much in federal taxes that year, or otherwise, they could carry forward and utilize against federal tax liability in future years.

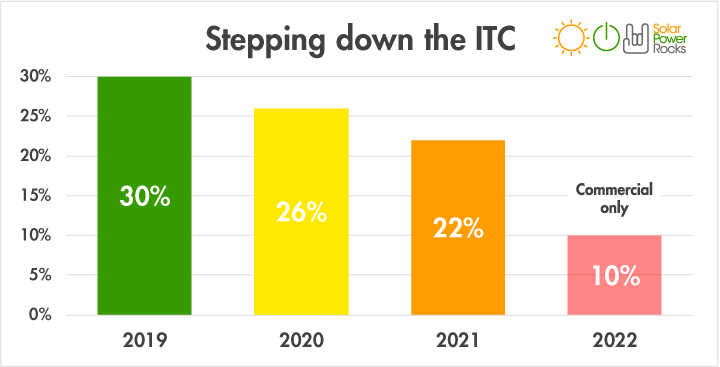

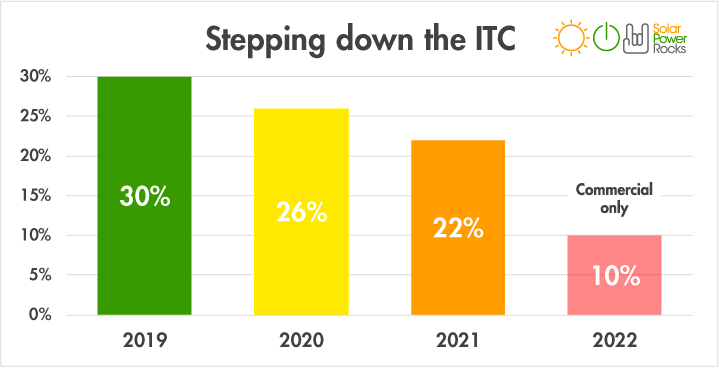

Congress has previously extended the ITC multiple times, most recently at the end of 2015 when the ITC was slated to drop down to 10%. That extension is when the current step-down levels were set, which are summarized below. Starting in 2020, the ITC is slated to step-down to the 26% level for both commercial and residential projects.

Key Provisions:

- 2019: full 30% tax credit applies only to commercial projects that commence construction before 1/1/2020

- 2019: full 30% eligibility applies to residential projects placed in service (PIS) before 1/1/2020

- 2020: tax credit reduces to 26% for residential and commercial customers

- 2021: tax credit reduces to 22% for residential and commercial customers

- 2022: and beyond: tax credit reduces to 10% for commercial customers. There will be no federal tax credit for residential solar+storage systems owned by homeowners for 2022 and beyond

- “Commence construction” language: the IRS issued a clarification on ITC eligibility to allow projects that start the construction process before the end of the year to qualify for ITC that year.

What’s the net effect?

The ITC stepdown and reduced tax credit rate is obviously detrimental to the project economics of a solar and/or storage project. Given that this is a federal tax credit, this would apply to projects in all 50 states. To give a quick example, for a $40,000 residential solar and energy storage project, the ITC reducing from 30% to 26% in 2020 would be a $1,600 reduction in tax credit, which would extended out the payback period, and reduce the project Return on Investment (ROI) Internal Rate of Return (IRR), and Net Present Value (NPV). We will explore this in more depth in an upcoming blog.

The silver lining of the ITC step-down from the perspective of solar and energy storage developers and salespeople is that a declining incentive always creates more imperative to buy. Potential customers are now incentivized to move quickly in committing to a project, in order to capture the full 30% ITC before years’ end, which will repeat itself each year before the next tier step-down. This will likely cause strong demand and an influx of projects looking to commence construction before the end of the year. Ironically this could lead to developers increasing prices as their project construction pipelines approach capacity.

Updates in Energy Toolbase:

Energy Toolbase has added all of the upcoming ITC step-down incentives into our database through 2022. This includes separate incentives ITC incentives for residential, commercial and energy storage projects. Note: we recently activated the “2020 – 26% ITC” incentives, so these will show up as selectable options in “Step 3 – Incentives”. For non-Residential projects that have longer project sales cycles and lead times it may be most appropriate to begin modeling with the “2020 – 26% ITC”.